Junk Bonds have had a massive comeback over the last, eeeeerr, yes ever since the FED started injecting liquidity! A lot of issues went from 20-30 cents back to or at least close to par. What a miraculous recovery that has been...

click on the chart to enlarge

Rightly John Hussman is pointing out this week that Bernanke is leaping into the liquidity trap . Because the theoretical godfather himself knew:

"There is the possibility... that after the rate of interest has fallen to a certain level, liquidity preference is virtually absolute in the sense that almost everyone prefers cash to holding a debt at so low a rate of interest. In this event, the monetary authority would have lost effective control."

John Maynard Keynes, The General Theory

Well, for now markets tell us that it is still a bit of a way towards this situation but thanks to the FED's fight fire with more fire approach to the debt issue TMN is certain we are headed this way if these guys do not get stopped either by the people or the government bond market. I mean, let's face it, risk premia are on the way to disappear again, as effectively there is no risk in holding a debt instrument.

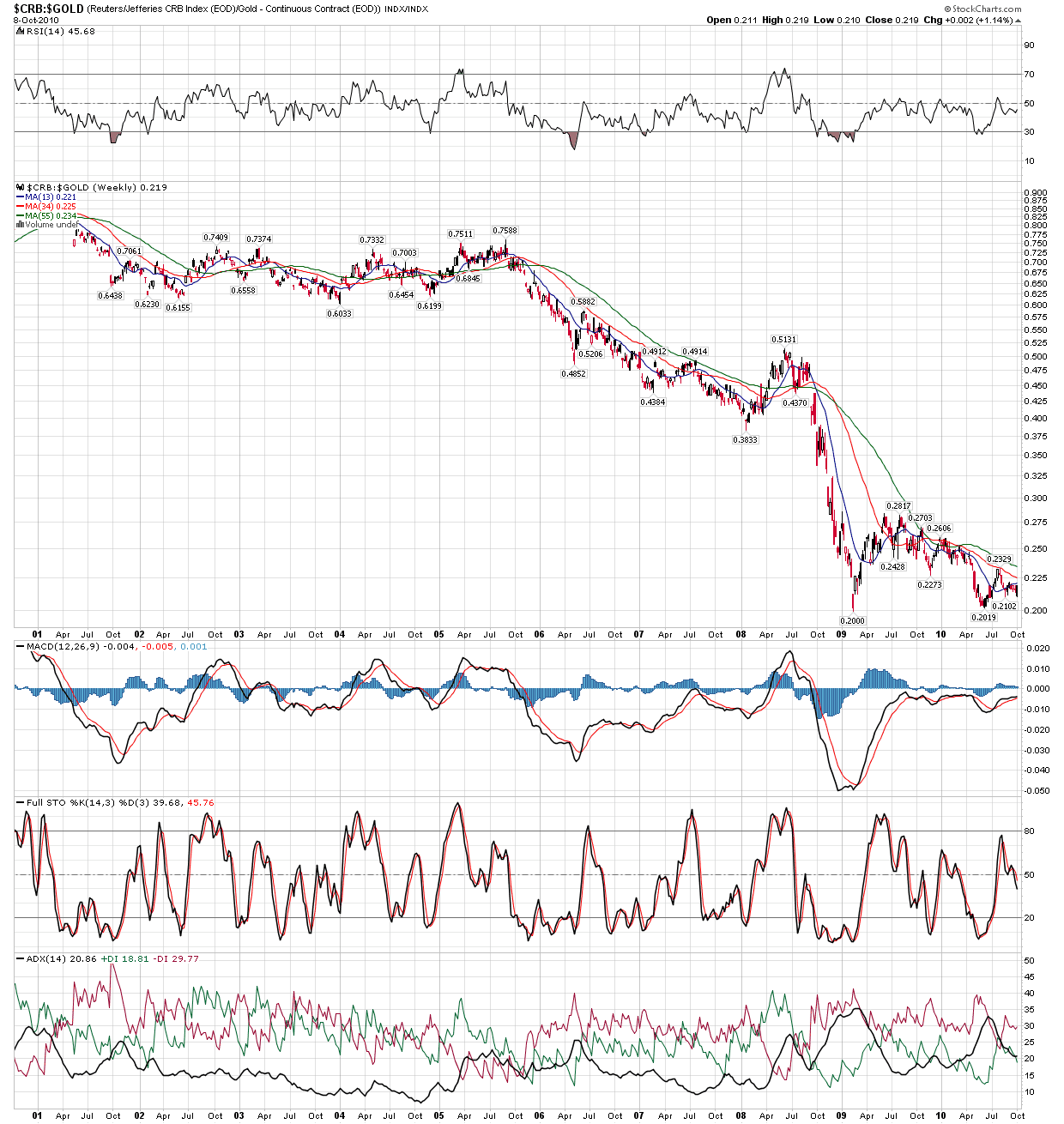

As there seems to be no risk, but also no yield any more, TMN's natural thought must be: why bother with all this if there is no risk, no fun and potentially a big headache involved. Is this what the chart below is telling us?

click on the chart to enlarge

Unfortunately this is only yesterday's chart, however, today this ratio is about 2% down on the day. Please note that more often than not, when this ratio trades lower, there is a heavy deflationary sell off across asset classes happening at some point. Whereas, when you see this ratio headed higher chances are that not only government bonds are outperforming the USD but many other asset classes, too.

The turn higher from June 2010 has got to go down in history as the period where even the dead had one last dance. TMN was not a market participant in 1987 but people that have been claim that one could have bought anything and it would have made money back then. Rings a bell?

Anyhow, this chart now is suggesting that there is a chance market participants are swapping "hope" for cash. Precious metals seem to be getting some attention on the back of this (why bother with any paper??), as both Gold and Silver are up today but it could be a matter of time until also these two fall victim to short term liquidity needs. TMN would not short them outright, will stay short bonds though until further notice instead.

{kind=link}